![]()

How to Set Financial Goals and Actually Achieve.

Most people want to be better with financial goals. However, wanting something and actually making it happen are two very different things.

Here is the honest truth — without clear financial goals, your money has no direction. It just flows in, flows out, and disappears. Month after month. Year after year. And one day you look back and wonder where it all went.

The good news? Setting financial goals is not complicated. In fact, it is one of the simplest yet most powerful things you can do to completely change your financial life. Furthermore, you do not need a huge income or a finance degree to make it work.

By the end of this guide, you will know exactly how to set financial goals that are realistic, motivating, and — most importantly — actually achievable. So let us get into it.

Table of Contents

- What Are Financial Goals and Why Do They Matter?

- Types of Financial Goals — Short, Medium, and Long Term

- The SMART Framework — The Right Way to Set Financial Goals

- Financial Goals Examples for Every Stage of Life

- How to Prioritize Your Financial Goals

- Step-by-Step Plan to Actually Achieve Your Financial Goals

- The Biggest Mistakes People Make With Financial Goals

- How to Stay Motivated and on Track

- Financial Goals FAQ

- Final Thoughts + Action Plan

What Are Financial Goals and Why Do They Matter?

Financial goals are simply a target you set for your money. It could be saving $1,000 in the next three months. It could be paying off your credit card debt by the end of the year. It could be retiring comfortably at 60. Whatever the target is, it gives your financial decisions a clear purpose.

Think of it this way. Imagine getting into a car with no destination in mind. You drive around, burn fuel, and eventually run out of gas — with nothing to show for the journey. That is exactly what happens when you manage money without goals. You earn, you spend, you repeat, and you never actually get anywhere meaningful.

On the other hand, when you set clear financial goals, something powerful happens. Every spending decision becomes easier. Every savings contribution feels purposeful. And over time, the results compound into real, life-changing progress.

Why Financial Goals Are More Important Than Ever in 2026

The economic landscape in 2026 is not forgiving. Rising living costs, shifting job markets, and increasing financial complexity mean that hoping for the best is simply not a strategy anymore. Moreover, research consistently shows that people who write down their goals are significantly more likely to achieve them than those who keep everything in their head.

Furthermore, financial security is directly linked to mental and physical health. When your money is under control, your stress levels drop. Your relationships improve. Your confidence grows. In short — financial goals are not just about numbers. They are about building a life you actually enjoy.

Types of Financial Goals — Short, Medium, and Long Term

Before you start setting goals, it helps to understand that not all financial goals are the same. In fact, they fall into three clear categories — and you need all three working together.

Short-Term Financial Goals (0–1 Year)

Short-term goals are things you want to accomplish within the next twelve months. Because they are close in time, they tend to feel more urgent and motivating. Additionally, achieving short-term goals builds the confidence and momentum you need to tackle bigger ones.

Examples of short-term financial goals:

- Building a $1,000 starter emergency fund

- Paying off one credit card completely

- Saving for a planned vacation without going into debt

- Cutting monthly expenses by $200

- Creating and following a monthly budget

Medium-Term Financial Goals (1–5 Years)

Medium-term goals sit in the middle ground — big enough to require sustained effort, but close enough to feel real. These goals often require consistent, disciplined action over months or years.

Examples of medium-term financial goals:

- Saving a full 3–6 month emergency fund

- Paying off all consumer debt

- Saving a down payment for a house

- Building a $10,000 investment portfolio

- Reaching a specific net worth target

Long-Term Financial Goals (5+ Years)

Long-term goals are the big ones. These are the goals that shape the overall direction of your financial life. Although they require patience, they are also the most transformative.

Examples of long-term financial goals:

- Retiring comfortably at your target age

- Paying off your mortgage early

- Building generational wealth for your children

- Achieving complete financial independence

- Funding your children’s college education

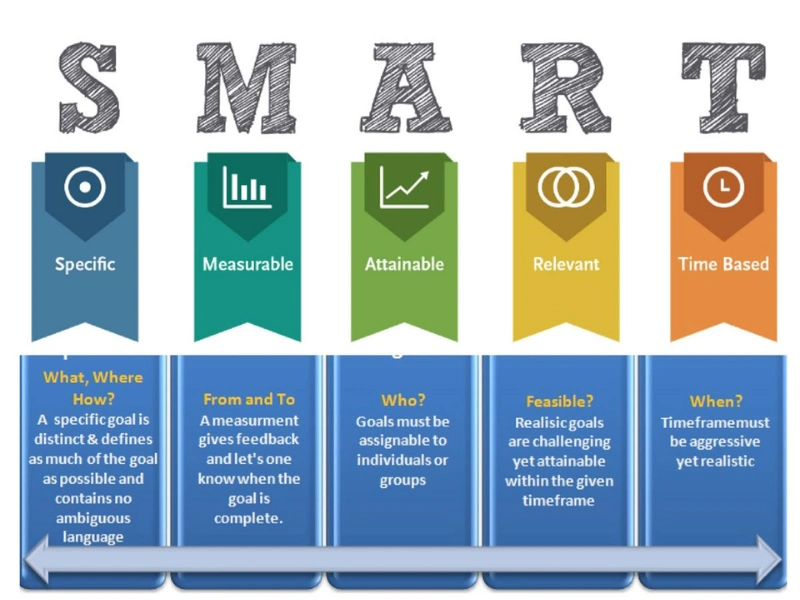

The SMART Framework — The Right Way to Set Financial Goals

Here is where most people go wrong. They set goals that sound good but are practically useless.

“I want to save more money.” — Not a goal. That is a wish. “I want to invest someday.” — Not a goal. That is a vague idea.

Goals without specifics do not work. Consequently, the most effective goal-setting method used by financial experts worldwide is the SMART framework. Let us break it down clearly.

S — Specific

Your goal must answer the question: exactly what am I trying to accomplish?

- ❌ “I want to save money”

- ✅ “I want to save $5,000 in a high-yield savings account”

M — Measurable

You must be able to track your progress with a clear number or milestone.

- ❌ “I want to get out of debt”

- ✅ “I want to pay off $8,000 of credit card debt”

A — Achievable

Your goal should stretch you — but not break you. An unrealistic goal is demotivating, not inspiring.

- ❌ “I will save $3,000 per month on a $3,500 monthly income”

- ✅ “I will save $400 per month starting this paycheck”

R — Relevant

Your goal should align with what actually matters to your life right now.

- ❌ Setting a retirement savings goal before you have paid off high-interest debt

- ✅ Prioritizing debt payoff first, then building retirement savings

T — Time-Bound

Every goal needs a deadline. Without a deadline, there is no urgency — and without urgency, there is no action.

- ❌ “I want to save for a house someday”

- ✅ “I want to save $20,000 for a house down payment by December 2027”

SMART Goal in Action — Real Example

Instead of: “I want to get better with money”

Write this: “I will save $300 per month automatically into a separate savings account and reach $3,600 in savings by December 31, 2026.”

That single sentence gives you a specific target, a measurable number, an achievable monthly amount, a relevant purpose, and a clear deadline. [That is the power of SMART goal setting](https://Investopedia.com/SMART goals).

Financial Goals Examples for Every Stage of Life

One of the biggest challenges with financial goals is knowing which ones to set. Therefore, here are practical, real-world examples broken down by life stage.

In Your 20s — Build Your Foundation

Your 20s are about building habits and foundations that compound over decades. Consequently, even small actions now pay enormous dividends later.

- Build a $1,000 starter emergency fund within 3 months

- Pay off student loan debt within 5 years

- Start contributing to a retirement account — even just $50 per month

- Create and follow a monthly budget consistently for 6 months

- Build credit score above 700

In Your 30s — Accelerate and Protect

By your 30s, income typically rises — but so do responsibilities. Therefore, this is the time to accelerate savings while protecting what you have built.

- Fully fund a 3–6 month emergency fund

- Maximize retirement contributions each year

- Save for a home down payment if homeownership is a goal

- Eliminate all high-interest consumer debt

- Get proper life and disability insurance in place

In Your 40s — Build Wealth Aggressively

Your 40s are often peak earning years. As a result, this is the time to build wealth seriously and close the gap on any retirement savings you missed in earlier years.

- Max out retirement accounts (401k, IRA, or equivalent)

- Pay off your mortgage aggressively

- Build a taxable investment portfolio

- Diversify income with investments or side income

- Review and update your estate plan

In Your 50s and Beyond — Protect and Transition

As retirement approaches, the focus shifts from growth to protection and transition planning.

- Ensure retirement accounts are on track for your target retirement date

- Eliminate all remaining debt before retirement

- Create a clear retirement income plan

- Review healthcare and insurance coverage thoroughly

- Consider legacy and estate planning goals

How to Prioritize Your Financial Goals

Once you know what your goals are, the next challenge is figuring out which ones to tackle first. After all, you cannot do everything at once. Therefore, here is a simple priority order that financial experts widely recommend.

Step 1 — Build a starter emergency fund ($500–$1,000) This comes first. Before anything else. Without a basic buffer, one unexpected expense will derail every other goal you set.

Step 2 — Pay off high-interest debt Credit card debt at 20–25% interest is mathematically destroying your wealth. Moreover, no investment reliably returns 20% per year. So pay off high-interest debt aggressively before investing heavily.

Step 3 — Build a full emergency fund (3–6 months of expenses) Once high-interest debt is gone, complete your emergency fund. This creates the financial stability you need to pursue every other goal with confidence.

Step 4 — Save and invest for medium and long-term goals Now comes the wealth-building phase. Contribute to retirement accounts, build an investment portfolio, save for a home — depending on what matters most to your life at this stage.

Step 5 — Build generational wealth and advanced goals Once the foundations are solid, focus on legacy, estate planning, and advanced financial goals.

Step-by-Step Plan to Actually Achieve Your Financial Goals

Setting goals is the easy part. Sticking to them is where most people struggle. Therefore, here is a clear, practical plan to turn your goals from intentions into results.

Step 1 — Write Every Goal Down

Research consistently shows that writing down your goals makes you dramatically more likely to achieve them. Do not keep your financial goals in your head — write them down on paper, in a journal, or in a notes app. Then place them somewhere visible. Your bedroom mirror. Your phone wallpaper. Your desk.

Visibility creates accountability. And accountability creates results.

Step 2 — Break Big Goals Into Monthly Milestones

A goal of saving $12,000 sounds massive. However, saving $1,000 per month for 12 months sounds completely achievable. The math is identical — but the psychology is completely different.

Break every large goal into monthly milestones. Then break monthly milestones into weekly actions. Suddenly, the biggest goals in your life become a series of small, manageable steps.

Step 3 — Automate Everything Possible

Motivation fades. Discipline has bad days. However, automation never misses a transfer.

Set up automatic transfers for savings, automatic payments for debt, and automatic contributions to investment accounts. When progress happens automatically in the background, you remove the biggest obstacle to achieving financial goals — which is simply forgetting or delaying.

Step 4 — Track Your Progress Monthly

What gets measured gets managed. Therefore, once a month, sit down and review your numbers honestly.

- How much did you save this month?

- Did you hit your milestone?

- If not, what got in the way?

- What will you do differently next month?

This monthly check-in takes about fifteen minutes and makes an enormous difference in your long-term results.

Step 5 — Celebrate Small Wins

Financial goal achievement is a long journey. Consequently, celebrating milestones along the way is not optional — it is essential. It keeps you motivated for the long road ahead.

Paid off your first credit card? Celebrate it. Hit your first $1,000 in savings? That deserves recognition. The celebration does not need to be expensive. It just needs to be meaningful.

Step 6 — Adjust When Life Changes

Life is unpredictable. Job changes, family events, health issues, and economic shifts all affect your financial picture. Therefore, treat your financial goals as living documents — not stone tablets.

Review and adjust your goals every quarter. If something is no longer realistic, change it. If you achieved something ahead of schedule, set a new target. Flexibility keeps you in the game long-term, whereas rigidity often leads to giving up entirely.

The Biggest Mistakes People Make With Financial Goals

Even the most motivated people stumble because of avoidable mistakes. Here are the most common ones — and exactly how to avoid each one.

Mistake 1 — Setting Too Many Goals at Once

Trying to save, invest, pay off debt, and plan for retirement all at the same time leads to overwhelm and paralysis. Instead, focus on one or two primary goals at a time. Finish them, then move to the next ones.

Mistake 2 — Making Goals Too Vague

“Save more” and “spend less” are not goals. They are intentions. Without specific numbers and deadlines, vague goals disappear within weeks. Always use the SMART framework when writing your goals.

Mistake 3 — Not Accounting for Irregular Expenses

Most people budget for monthly expenses but forget about irregular ones — car registration, annual subscriptions, holiday spending, medical bills. Consequently, these expenses feel like emergencies and derail savings goals. Anticipate them. Budget for them. Set money aside monthly for irregular annual expenses.

Mistake 4 — Giving Up After One Setback

Missing a monthly savings target does not mean your goal is over. Furthermore, dipping into your savings for a genuine emergency does not mean you failed. Setbacks are a normal part of any long financial journey. What matters is getting back on track the following month — not giving up altogether.

Mistake 5 — Never Reviewing or Updating Goals

Goals set in January are often forgotten by March. Regular reviews — at least once per quarter — keep your goals alive and relevant. Without reviews, even the best financial plan becomes outdated and disconnected from your real life.

How to Stay Motivated and on Track

Motivation naturally ebbs and flows over long financial journeys. Therefore, here are proven strategies to keep yourself moving even on the hard days.

Visualize your future clearly. Before every major spending decision, picture your life when you achieve your financial goals. The debt-free feeling. The retirement freedom. The security of a fully funded emergency fund. That picture is worth more than any impulse purchase.

Find an accountability partner. Share your goals with someone you trust — a spouse, a friend, or an online community. Knowing that someone else is watching your progress creates powerful motivation to follow through.

Use a progress tracker. Whether it is a simple spreadsheet, a budgeting app, or a handwritten chart on your wall — visual progress is deeply motivating. Watching a savings bar fill up or a debt number decrease keeps you engaged and energized.

Remember your “why.” Every financial goal has a deeper reason behind it. Security. Freedom. Family. Peace of mind. When progress feels slow, reconnect with that deeper reason. It will keep you going longer than any short-term motivation trick ever could.

Financial Goals FAQ

How many financial goals should I have at one time? Focus on one to three active goals at a time. More than that splits your attention and resources too thin. Once you achieve a goal, add the next one from your list.

What is the most important financial goal to start with? Building a starter emergency fund of $500–$1,000 is almost always the right first step. Without it, every other financial plan is vulnerable to being derailed by the first unexpected expense.

How do I set financial goals if my income is irregular? Use your lowest-income month as your baseline for goal calculations. In higher-income months, send the extra directly toward your goals. Furthermore, build a larger emergency fund — 6 to 12 months of expenses — to provide a buffer during slow months.

Should my partner and I set financial goals together? Absolutely. In fact, shared financial goals significantly reduce money-related conflict in relationships. Set aside time together to discuss and align on priorities. Working toward the same goals as a team is far more powerful than working independently.

How often should I review my financial goals? At minimum, review them every quarter. Additionally, review them after any major life change — new job, marriage, new child, health event, or significant income change.

What if I miss a milestone or fall behind? Adjust and continue. Missing one milestone does not mean the goal is over. Recalculate your timeline, increase your monthly contribution if possible, and keep moving. Consistency over the long run matters far more than perfection in any single month.

Final Thoughts + Your Action Plan for Today

Here is the truth about financial goals — most people know they need them. But most people also keep putting them off until the timing feels right.

The timing will never feel perfect. There will always be something more urgent, more expensive, or more distracting. Consequently, the best time to set your financial goals is always right now — with whatever information, income, and energy you have today.

You do not need a perfect plan. You do not need a huge income. You do not need to figure everything out at once. You just need to start.

Here is your action plan for today:

- Write down one short-term financial goal using the SMART framework

- Calculate exactly how much you need to save or pay each month to hit it

- Set up one automatic transfer toward that goal — even if it is just $25

- Put a quarterly review date in your calendar — right now, before you close this tab

That is it. Four steps. Fifteen minutes. And the beginning of a completely different financial future.

What is your number one financial goal for 2026? Share it in the comments below — let us keep each other accountable.